We wanted to provide an update in regards to the current COVID-19 situation. Firstly however I would like to extend my best wishes to you and your family during these difficult times. Please rest assured that we will be doing everything we can to accommodate you and to ensure continuity of service during this period.

QuickFile is a cloud based digital platform, our infrastructure and procedures are designed to handle these types of situations. Our teams are already distributed and we envisage no disruption to service during the period of lockdown. Furthermore our support teams will be onhand to assist you with any questions you may have during this deveoping situation.

Supporting you and your business

The UK Government has implemented some help for businesses in light of the threat from COVID-19. This post will highlight some of the places business owners can go to get access to this help.

This help includes:

- Coronavirus Job Retention Scheme

- Statutory Sick Pay relief package for SMEs

- Deferring VAT and Income Tax payments

- HMRC Time To Pay Scheme

- Small business grant funding of £10,000 for all businesses in receipt of small business rate relief or rural rate relief

- 12-month business rate holiday for all retail, hospitality, and leisure businesses in England

- Business rate holiday for nurseries

- Grant funding of £25,000 for retail, hospitality and leisure businesses with a rateable value between £15,000 and £51,000

- Coronavirus Business Interruption Loan Scheme offering loans of up to £5 million for SMEs through the British Business Bank

- A new lending facility from the Bank of England to help support liquidity among larger firms

Coronavirus Job Retention Scheme

Under this scheme, all UK employers will be able to access support to continue paying part of their employees salary up to 80%, capped at £2,500 per month. This is for employees who would otherwise have been laid off during the crisis.

Eligibility

All UK businesses are eligible.

How to access the scheme

You will need to do the following:

-

Designate affected employees as ‘furloughed workers’ and notify your employees of this change.

-

Changing the status of employees is still the subject of existing employment law and may be subject to negotiation.

-

Submit information to HMRC about the employees that have been furloughed and their earnings through a new online HMRC portal

HMRC are currently working on setting up a new system for reimbursement, existing systems are not set up to facilitate payments to employers.

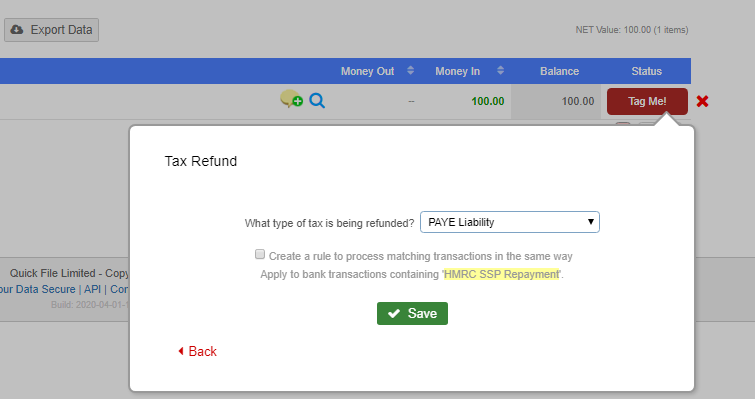

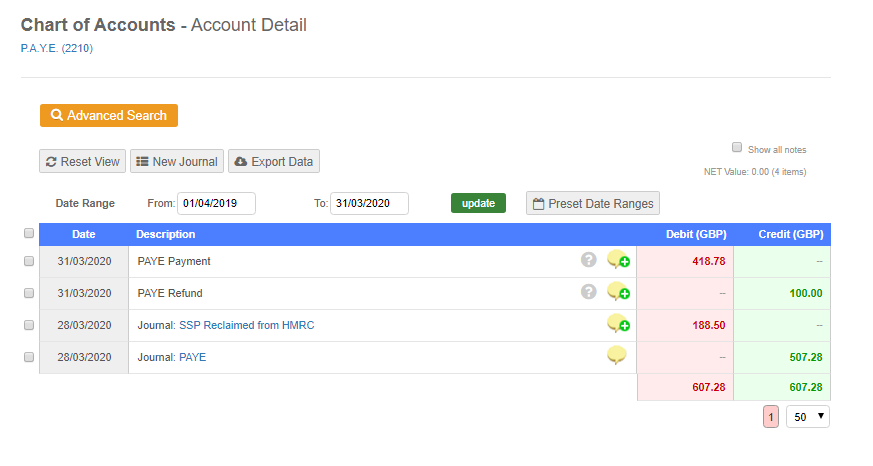

For businesses who are paying sick pay to employees

Legislation is being brought forward that allows SMEs and employers to reclaim Statutory Sick Pay (SSP) paid for sickness absence due to Codiv-19. There is an eligibility criteria that will have to be followed:

-

The refund will cover up to 2 weeks’ SSP per eligible employee who has been off work due to Covid-19.

-

Employers with fewer than 250 employees will be eligible

-

- Based on the number of employees as of 28th February 2020.

-

Employers will be able to reclaim expenditure for any employees who have claimed SSP as a result of Covid-19.

-

Employers should keep a record of staff absences and payments of SSP, employees will not need to provide a GP fit note.

-

If employers require evidence, any employees suffering from the symptoms of Covid-19 can get an isolation note from NHS 111 online.

-

The government will work with employers over the coming months to set up the repayment mechanism.

Eligibility

You are eligible if your business

- Is based in the UK, and

- Is an SME with less than 250 employees (as of 28th February 2020)

How to access the scheme

A rebate scheme is being developed, further details will be released in due course.

Deferring VAT and Income Tax Payments

Businesses will have their VAT payments deferred for 3 months. If you’re self employed, Income Tax payments due in July 2020 will be deferred until January 2021. It’s anticipated that further measures for self employed will be announced this week.

VAT

The deferral will apply from 20th March 2020 until 30th June 2020.

Eligibility

All UK businesses are eligible.

How to access the scheme

This is an automatic offer - no application is required. Businesses will not need to make a VAT payment during this deferral period. Tax payers will be given until the end of the 2020/2021 tax year to pay any liabilities that have accumulated during the deferral period. VAT refunds and reclaims will be paid by the government as normal.

Income Tax

Income Self-Assessment payments due on 31st July 2020 will be deferred until 31st January 2021.

Eligibility

If you are classed as self-employed, you are eligible.

How to access the scheme

This is an automatic offer, there is no need to apply for it.

There are no penalties or interest for late payment during the deferral period.

Businesses paying tax: Time To Pay Service

All businesses and self-employed people in financial distress, and with outstanding tax liabilities, may be able to receive support with their tax through HMRC’s Time To Pay Service.

These arrangements are agreed on a case-by-case basis and are tailored to individual circumstances and liabilities.

Eligibility

You are eligible if your business:

- Pays tax to the UK government

- Has outstanding tax liabilities

How to access the scheme

If you have missed a tax payment, or you might miss your next tax payment due to Covid-19, please call HMRC’s dedicated helpline: 0800 0159 559.

If you’re worried about a future payment, please wait until nearer the time before making contact.

Retail, Hospitality and Leisure businesses’ business rates

A business rates holiday will be introduced for retail, hospitality and leisure businesses in England for the 2020/2021 tax year.

Businesses that received the retail discount in the 2019/2020 tax year will be rebilled by their local authority.

Eligibility

You are eligible for the business rates holiday if your business is:

- Based in England

- In the retail, hospitality and / or leisure sector

Properties that will benefit from the rate relief will the occupied and wholly, or mainly be used:

- As shops, restaurants, cafes, drinking establishments, cinemas and live music venues

- For assembly and leisure

- As hotels, guest and boarding premises, and self-catering accommodation.

How to access the scheme

There is no action required to access the help, it will be applied on your next tax bill in April 2020. However, local authorities may have to reissue your bill automatically to exclude the business rate charge. This will be done as soon as possible.

Grant funding of £10,000

The government will provide an additional Small Business Grant Scheme for local authorities to support small businesses that already pay little or no business rates because of small business rate relief (SBBR), rural rate relief (RRR) and tapered relief. This will provide a one-off grant of £10,000 to eligible businesses to meet their ongoing business costs.

Eligibility

You are eligible if:

- Your business is based in England

You are a small business and already receive SBBR and / or RRR* You are a business that occupies a property

How to access the scheme

You do not need to do anything. Your local authority will write to you if you are eligible.

Any enquiries relating to eligibility or provisions of rates or the grant should be directed to your local authority.

Coronavirus Business Interruption Loan Scheme

The Coronavirus Business Loan Interruption Scheme supports SME’s with access to working capital, of up to £5 million in value and for up to 6 years.

The government will pay to cover the first 12 months of interest payments and any lender-levied fees. Meaning smaller businesses will not face any upfront costs and will benefit from lower initial repayments.

The government will provide lenders with a guarantee of 80% on each loan to give lenders further confidence in providing finance to SMEs.

This scheme is being delivered through commercial lenders, backed by the British Business Bank.

Eligibility

You are eligible for this if:

- Your business is based in the UK

- Your annual turnover is no more than £45 million

- Your business meets the other eligibility criteria set by the British Business Bank

How to access the scheme

The scheme is open for applications. To apply you should talk to your bank in the first instance, but you can also contact one of the 40 accredited finance providers. Contact them as soon as possible to discuss your business plan. You can find out the best way to contact them via their websites.

All major banks are offering this scheme. If you have an existing loan with monthly repayments, you may wish to ask for a repayment holiday to help with cash flow.

Business rate holiday for nurseries

A business rate holiday will be introduced for nurseries in England for the 2020/2021 tax year.

Eligibility

You are eligible if:

- Your business is based in England

Properties that will benefit from the relief will be:

- Occupied by providers on Ofsted’s Early Years Register

- Wholly or mainly used for the provision of the Early Years Foundation Stage

How to access the scheme

There is no action required to access the help, it will be applied on your next tax bill in April 2020. However, local authorities may have to reissue your bill automatically to exclude the business rate charge. This will be done as soon as possible.

Cash grants

The Retail and Hospitality Grant Scheme provides businesses in the retail, hospitality and leisure sectors with a cash grant of up to £25,000 per property.

For businesses in these sectors with a rateable value of between £15,001 and £51,000, they could receive a grant of £25,000.

Eligibility

You are eligible if:

- Your business is based in England

- Your business is in the retail, hospitality and / or leisure sector

Properties that will benefit from the rate relief will the occupied and wholly, or mainly be used:

- As shops, restaurants, cafes, drinking establishments, cinemas and live music venues

- For assembly and leisure

- As hotels, guest and boarding premises, and self-catering accommodation.

How to access the scheme

You do not need to do anything. Your local authority will write to you if you are eligible for this grant.

Any enquiries on eligibility for, or provisions of, the reliefs and grants should be directed to your local authority.

Larger firms - Covid-19 Corporate Financing Facility

Under this scheme, the Bank of England will buy short-term debt from larger companies. This will support your company if it has been affected by a short-term funding squeeze by allowing you to finance your short-term liabilities.

Eligibility

All UK businesses are eligible.

How to access the scheme

Information about how to access the scheme will be released shortly.

More information on the scheme is available from the Bank of England.

Summary

These are challenging times for all businesses, rest assured that we will be doing everything we can to assist you through this period.

Thank you for choosing QuickFile and please stay safe.

Best wishes

Glenn Drake

Co-founder

.

.