Hi. Amateur accountant here. I’m just trying to wrap my head around the correct way to enter/account corporation tax. I’ve found this thread which in theory makes sense to me however I am getting a little confused on the timings of it all.

If I’m interpretting it correctly, the process is that once you know the CT payable (which is calculated from the profit & loss for the year (?) ) you then journal the amount in the ledgers using a debit/credit to the 8500 Corporation Tax Charge for the Year and 2320 Corporation Tax. When you later make the payment and tag it to corporation tax, the balance is effectively zero’d.

However, as is stated, this CT expense is then entered into the Profit and Loss Account & Balance Sheet. But doesn’t that mean that the P&L account I just calculated the CT charge from has now changed?

Example:

£10k P&L account at year end with 20% tax rate = £2000 CT. However after jounral entries done, P&L Account is now £8k.

So when I fill out the CT600 what do I enter? If I enter a P&L account of £8k surely it is going to say my CT liability is £1600 not the £2000 I’ve already accounted for? Isn’t this a circular reference? P&L Account > CT > Expense > P&L Account … and so on.

My only conclusion is that you only apply the journal entry after you have submitted the CT600?

This is probably blindingly obvious to someone with an accounting background but I need some clarification please! Thanks!

Another way to put it would be - when I’m filling in my CT600 with my quickfile P&L report in front of me, should the CT charge expense (assuming I have worked it out myself) for the year being submitted be on the report ?

Or, upon completion and submission of the CT600 where it has calculated the tax I owe, do I then create the journal entries for the CT charge, thus excluding it from the submitted CT600.

You may not get a great response here with this being more skewed towards accounting methodology. I will however leave the post open for others to comment.

Right. My understanding from some helpful (and some unhelpful) feedback from accountingweb/uk business forums is that CT tax charges are taken into account on the CT600 but it isn’t tax deductable so shouldn’t impact the P&L account.

However from my P&L sheet it clearly is factored into the net profit value. Can anyone explain to me how this is properly accounted for? Do I need to factor it into an adjustment somewhere?

Hi Glenn

I have been meaning to raise this point, didn’t get a chance until now.

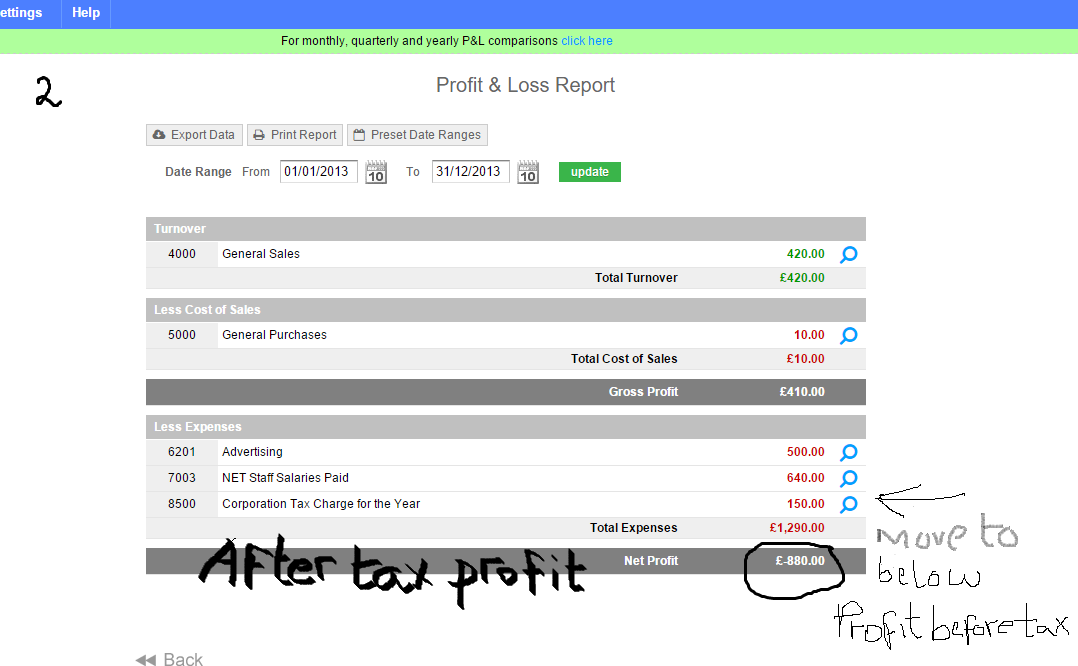

The thing is, Corporation tax is calculated on ‘profit before tax’. So as soon as the corporation tax figure is inserted by journal, it sits in the profit and loss where we can’t distinguish before and after tax profit figure.

I think, the tax summary on QF also tends to pick up after tax profit and calculates estimated CT on after tax profit. Which is why i wanted to point this out.

I think the solution will be to include the CT after the profit figure and name the new balance as after tax profit.

See screenshots below.

This is probably causing the confusion with Roshawk…

Would really appreciate if you could look into it, many thanks

in the tax summary, the CT will then always be calculated on profit before tax figure and profit available for distribution/dividends will be calculated from after tax profit figure.

On a separate note, i noticed in the tax summary, that dividends available for distribution is for the current accounting year only. Once the above is implemented i.e. profits after and before tax, can we have calculations for profit available for distribution for all available accounting years?

Something you could look into after the above please? Many thanks

I can’t promise anything at this stage, we are very committed to a range of other projects, but as with all areas of development if it’s something we are getting asked for frequently we will prioritise.