I have a new employee who was due a tax rebate the first time I ran payroll for them. HMRC paid me the rebate which I processed as PAYE refund and then the payment to the employee as net salary paid. When I run the P&L the salary is showing but the PAYE refund isn’t so it is skewing my monthly P&L - is this the correct approach?

You say “net salary paid” which suggests you aren’t using payroll journals, so how do you normally account for tax and NI deductions from your employees’ wages? Usually if you have any tax or NI to deal with it’s better to turn “post net wages to balance sheet only” to “ON” in your QuickFile settings and then make a proper journal from the numbers generated by your payroll software.

Typically each payroll run would give rise to a journal that does P&L debit entries on gross wages and employer’s NI and pensions (if applicable) and balance sheet credit entries on PAYE (for tax and employee NI deductions, plus employer NI contributions and anything else that you pay to HMRC via pay-as-you-earn), any pension liabilities (employer and employee) and Net Wages (for the amount left over after deductions, which you pay to the employee). When you tag the payment to the employee that debits to net wages and when you make the monthly/quarterly payment to HMRC for PAYE that debits the PAYE nominal to settle that liability and the same for your pension payments if any.

When your payroll software generates a tax refund your journal will have the usual gross wages P&L line but this time the PAYE balance sheet line will be a debit (asset) rather than a credit (liability to HMRC), and the net wages credit will be higher than the gross wages debit to balance things out. Paying the employee is exactly the same as usual - tag the transaction to net wages to balance out the credit from the journal, and the tax rebate from HMRC becomes a credit on the PAYE nominal to cancel out the debit balance from the journal.

1 Like

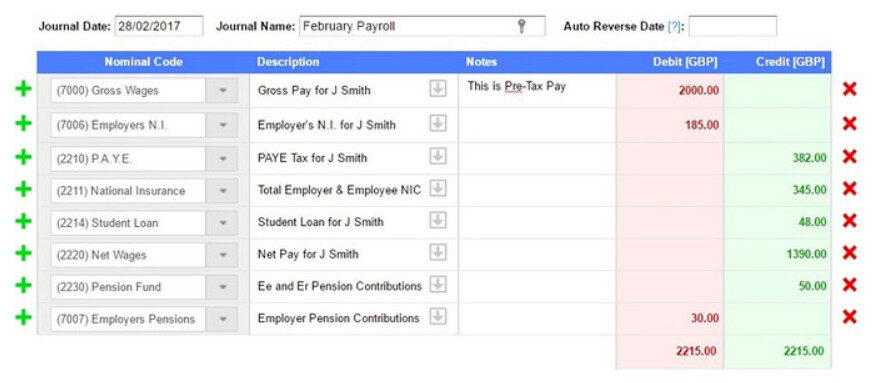

Just to add to Ian’s reply, turning on the setting ‘post to balance sheet only’ makes sense and there is a QF knowledge base guide at this link:

https://support.quickfile.co.uk/t/recording-payroll/16003

and it shows the type of journal you could use:

This will show the liability until payment, but I’m not sure that using QF’s procedure for payment will clear the liability accounts.

In the example, there is a liability of

made up of codes:

When you record a bank payment and record it as per the guide,

I’m not sure that QF deals with the whole situation when it processes the transaction shown above.

It may post to Net Wages (2220) but what about the other liabilities?

.

…

Firstly there’s no point splitting up the pay-as-you-earn liabilities for tax, NI and student loan into separate nominals - they are all part of your single PAYE liability to HMRC so they can all go to the same 2210. The dedicated NI and student loan nominals are only needed for liabilities that are not settled through the PAYE system (e.g. class 1A).

With that the handling of the various liabilities is simple

- tagging as “salary/wages” offsets the liability in 2220

- tagging as “tax payment to HMRC” and selecting the “PAYE” option offsets 2210

- when you pay over pension contributions to the pension provider tag as “something not on the list” and choose the 2230 code

Yes, good point.

If what you say was added to the guide, it could be quite useful to people.

.

This topic was automatically closed after 7 days. New replies are no longer allowed.