Hi,

The answer to your query is somewhat involved, but I’ll try to keep it brief!

If a company purchases equity in other companies, how they are recognised and valued depends on whether the buyer intends to hold the investment for the long term, or to ‘trade’ the investment for in the short term.

If the investment is planned to be ‘traded’ in the short tern then it is recorded in the accounts as what is known as Fair Value through Profit or Loss (FVTPL).

If for the long term, it can be, if so wished, recorded as Fair Value through Other Comprehensive Income (FVTOCI).

The buyer is supposed to make the choice between FVTPL or FVTOCI when making the investment and it is not supposed to be changed, it is supposed to be an irrevocable option.

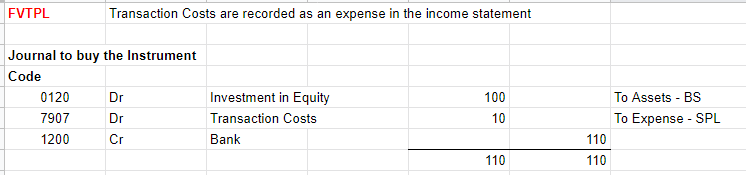

On a bookkeeping level, the difference between FVTPL and FVTOCI is that if using FVTPL then the transaction costs (broker fees) are treated as an expense on the SPL, whereas in FVTOCI transaction costs are added to the opening value of the investment.

To give an example, say you had this:

To record this in QF I would make two new chart of account codes.

Then to record the investment using FVTPL you can do this:

Or to record the investment using FVTOCI you can do this:

At your year end, the value of your holdings would be found using fair value and gains or losses would be accounted for at that time.

Last thing to note, investments in derivatives are always treated as FVTPL.

Sorry it wasn’t so brief after all !!

Hope this helps a bit