The actual VAT paid on Gross income @11.5% is 1373.23.

I suppose my questions are as follows:

How do I keep ta running tab on actual VAT paid ? The Tax summary report doesn’t tell me . I don’t know why as though I’m cash accounting and it works on invoices , my cash register entries do produce an invoice(@20%) . I’m aware of the periodic BETA report

2 Is the total turnover reported £9,950 the figure that would actually be used in my accounts. This of course results in me keeping the difference between $1,990.20 and 1373.23 ?

I’m sorry for all these questions , it seems I’m doing a crash course in accountancy. I ask as when periodic reporting comes along I am considering doing my all my own returns. At the very least I need to understand how the software is working, come what may we will all be pushed into complete digital record keeping/bookkeeping and this software is definitely my preferred option long term and though I don’t really need most of the functionality at present it would be wise to get to grips with everything before it’s needed.

I am a new user as of yesterday. Im not an accountant but am trying to learn the same things as you myself.

You problem seems similar to mine. I assume your total Income is total (gross) sales income. Your basic overall problem, I feel, is the auto calculation of VAT.

Regarding your figures, your Total income is not “charged at 11.5%”. If my understanding is correct, the 11.5% VAT is already within that £11941.14 sum and should equal £1231.60 ( 11941.14/111.5 x100 = 10709.54; i.e. your net sales income, then subtract this from total (gross) Income £11941.14 to get correct VAT of £1231.60 ); i.e. your actual VAT of £1373.23 is wrong. VAT is calculated from net not gross.

As far as i can see, implementing this math correction, at the detail QuickFile form entry level, is the only way to eradicate the difference between VAT sums that you mention (£1373.23 and £1990.20), i.e. all figures will then work up from the same detail whereas now, they don’t appear too. In short, your 4000 income / Total turnover will be corrected from £9950.94 to £10709.54 ( which will implement the correct VAT (£1231.60 ) which should then itself be incorporated into the sales VAT account 2200 ). This difference of £9950.94 minus £10709.54 = £758.6. This £758.60 sum increases your net turnover amount and, in essence, means your currently stated VAT sum will decrease as a liability but at the expense of a slightly increased ( total sales - total charged expenses ) income tax liability.

In summary, you’ll have to work out the correct VAT and deduct it backward from the gross income figure at the detail entry level then input it yourself and not let the system calculate it.

Hope that helps you as much as its helped me in determining my own way forward.

If you’re on a flat rate of 11.5% and not issuing real VAT invoices to your customers then I suppose you could record your sales in QuickFile at a fake VAT rate of 13%, which is roughly equivalent to the amount you’d pay on flat rate (13% of net is approximately equal to the 11.5% of gross that the flat rate calculation will compute).

If you do need to issue vat invoices then this won’t work as those have to say 20% as the VAT rate.

I knew I had read this somewhere; Seems for reporting purposes my turnover figure is - 20% VAT regardless of what I actually charge and I keep the difference. So perhaps the report is correct ?

" The VAT Flat Rate Scheme is designed to help simplify the VAT Return process for small businesses. It is intended to ensure businesses pay roughly the same amount of VAT without having to complete as much paperwork as other VAT schemes.

The Flat Rate Scheme enables businesses to keep the difference between the amount paid to HMRC and the amount of VAT charged to customers. However, unlike other schemes, businesses paying a flat rate cannot usually reclaim VAT on purchases, with the exception of some capital assets worth over £2,000."

Bill

£1373.23 as calculated by Quickfile and my spreadsheet is correct. I have been through this with Ian (see post ) and he is correct. I queried the same myself.

Sum is *11.5% on gross turnover

Further to my post I can confirm I do indeed keep the difference so P&L figure is technically correct. However that “kept” income has to be accounted for somewhere. This means that the VAT figures and turnover amounts in the P&L and trial balance will are not accurate reflections of the state of accounts for a flat rate business.

My accountant I would assume would correct this at the end of year accounts but I need to know the state of my business. I need to hand information to the accountant that accurately reflects trading. The options are it seems:

Quickfile to provide a way of showing a vat summary for flat rate payments , a true account of what has been paid.

A way of Showing “benefit derived from flat rate scheme” this would also help people to track if flat rate is working for them.

item 2 could then either be reflected in the accounts under some heeding or other or simply added back to turnover.

Hope all that makes sense , any suggestions for how this is achievable in Quickfile at present ?

When you run the VAT return in QuickFile we create a journal.

One of the lines in this journal would be to nominal 4999 Flat Rate VAT Sales, which is a sales nominal code. This would account for the additional turnover.

They are, but only at the end of a quarter once you have submitted the VAT return.

When you submit your VAT return in QuickFile it calculates the difference between the amount of VAT you collected in the quarter and the amount that you owe according to the flat rate calculation, and moves that to the “flat rate adjustment” nominal under the sales section (as a credit increasing your income if you owe HMRC less than you collected, as a debit decreasing it if you owe more - e.g. if you have a larger than usual value of zero rated sales). At that point your P&L up to the end date of that VAT quarter will be accurate.

Hi,

I ran a VAT return and downloaded a CSV file , no mention of it there. Are you saying that the journal is created when a bona fide return is filed ?

Ian, All sales are covered under flat rate , no zero etc. My turnover as we know is inclusive of VAT charged and VAT is a very simple calculation of *11.5% to determine VAT due . This we know. The calculations Quickfile is performing is to adjust 20% down to 11.5% correct ? and from what you and Matthew are saying the difference is reflected as a credit to the sales account ? Is this reflected in the sales and P&L to adjust income and also the trial balance . If I have understood this correctly my only way of keeping tabs on actual VAT paid would be these credits ?

Gosh this is a painful way of communicating:roll_eyes:

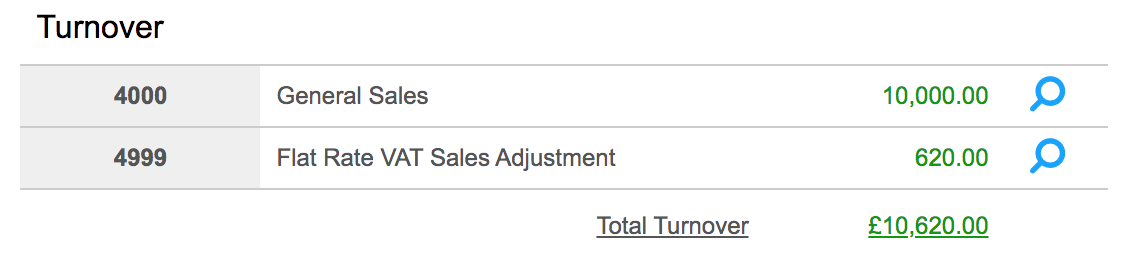

Pretty much, yes. Suppose for the sake of a simple example that you had recorded gross sales of £12,000 in a given quarter (as £10,000 net plus £2,000 VAT). This would show on your P&L as £10,000 general sales and on your balance sheet as £2,000 sales tax control. When you submit your VAT return it calculates that you owe £1,380 VAT to HMRC (11.5% of £12,000), so it creates a journal that does

debit £2,000 sales tax control

credit £1,380 VAT liability

credit £620 flat rate adjustment (4999)

If you now look at your P&L for the quarter it’ll show £10,000 general sales plus £620 FR adjustment, giving a turnover total of £10,620, and your balance sheet at the quarter end date will show £1,380 VAT liability that will be cancelled out when HMRC take the direct debit.

Right ok, so the above does this is and credits back to (Sales) 4999 does it actually show as a credit in the sales screen or simply added back in to turnover ?

debit £2,000 sales tax control - ok so takes the initial 20%

credit £1,380 VAT liability - credits the actual VAT back

The above does this

2200 Trial balance Sales Tax Control Account shows at 20%

Then Actual VAT liability replaces the 20% figure

And 2200 Balance sheet also shows the actual VAT

but all these figures only come correct after quarterly return.

I ask because the difference between the figures in your example (£620.00) is obviously income and will be reported as such . It would be nice if an actual entry is made as it would enable the user to gauge whether flat rate is working for them .

As you are aware for reporting purposes VAT of course is neither income nor an expense. Lots of accountants list it as an expense for ease of understanding of their clients or separate it out in notes on the account and I needed to know how Quickfile handled it.

HMRC give the following example

Example

A business has gross sales of £84,000 (including output VAT at 20% of £14,000), and expenses of £48,750 (including irrecoverable VAT). The flat rate VAT @ 6% is £5,040.

The accounts will show:

Turnover

£78,960

(£84,000 less £5,040 flat rate VAT)

Expenses

£48,750

Profit

£30,210

This of course reduces the turnover by flat rate and leaves the “difference” in turnover , This however does not enable at a glance assessment of benefit derived from being on the scheme.

Once again hope that makes sense and thank you for your patience Ian.

Where exactly do you mean by the “sales screen”? The “show all sales” list by default gives you the invoice totals including VAT, so even on normal VAT accounting you have to use the P&L report to see your position net of VAT.

In your specific case, if you are just using QuickFile to record your retail sales and you aren’t actually providing VAT invoices directly out of QuickFile to your customers (I believe this is the case from what you’ve said previously about operating a cafe with an electronic till), then you could minimise the amount of the 4999 adjustment by setting up a custom VAT rate of 13% under “additional sales VAT rates” in advanced settings.

If you record your gross retail sales as if they were inclusive of 13% VAT (e.g. instead of recording gross takings of £1200 as being £1000 net plus £200 VAT @ 20%, record it as £1061.95 net plus £138.05 VAT @ 13%), then your “general sales” on P&L should be approximately correct for a flat rate of 11.5% - the adjustment that QuickFile has to make on 4999 when you do a VAT return should be no more than a few pounds per quarter. This works because 11.5% of gross is equivalent to fractionally under 13% of net, and the adjustment ends up mostly just being the rounding error between the 13% calculation done on each invoice individually vs the 11.5% flat rate percentage calculated on the overall gross total for the quarter.

Thank you once again , Ok so the turnover question is sorted. And possibly your custom VAT solution is the answer, if I’m allowed to do that.

I’m wondering if I’m making a basic misunderstanding. HMRC state that you keep the difference between the VAT you charge and the flat rate you pay to HMRC. I’ve assumed that HMRC are saying between 11.5% and 20% . In other words for accounting purposes you are charging 20% . I have assumed this from the fact that my till receipt (invoice) must show 20% if requested. And that quick files defacto rate is 20%. From what your saying this is not the case.

This is important because :

I can’t possibly actually charge 20% as my prices would be to high

The difference between 11.5% and 20% would be credited back to turnover and if I haven’t actually added 20% to my prices then i’m out of pocket.

Maybe I should ask my accountant , I’m somewhat reluctant as he misinformed me about obligations under MTD , I’m looking for another at present

Well it looks like the flat scheme requires you charge standard VAT @20%/ hmm so there’s a conundrum for me. I have to find the sweet spot for what I actually charge which benefits me most . 20% is a definite no no

You have to itemise it as 20% VAT on your VAT invoices but that doesn’t necessarily mean you have to put your prices up by the full 20% - on standard VAT your inputs become cheaper because you can offset the VAT you paid to your suppliers against that which you collected from your customers so the effective cost to you of your inputs goes down. This effect is one of the reasons why they set different flat rates for different business types - some businesses have more deductible input tax than others on average.

As a cafe you’re unfortunately one of the worst hit by VAT registration since many of your inputs (your ingredients) are zero rated but you have to charge 20% on your outputs (food supplied in the course of catering is all 20% even if the same items would be 0% if supplied retail to take away). For you I guess it’s only confectionery, ice cream and soft drinks where you do pay VAT, plus your other overheads like energy bills.

It’s actually between 11.5% and 16.67%, because VAT is 20% (one fifth) of the net which is 16.67% (one sixth) of the gross. If the vat you would be eligible to reclaim on your purchases amounts to more than 5% of your gross turnover then you may be better off not using the flat rate scheme.

Hi Ian,

I was really talking about HMRC’s view point, in their view I charge standard 20% regardless of what I actually charge. This means the difference is credited to taxable turnover .If I cannot charge 20% then I somehow have to settle on a figure which offsets the increase in turnover (that I haven’t had. Either that or buy a bloody expensive oven to keep it out the taxmnans hands

Like I said on your previous thread, if you’re working on a flat rate of 11.5% of gross then you’d have to increase your retail prices by 13% to maintain the same gross profit percentage you have now.