If you cannot maintain your current workforce because your operations have been severely affected by Coronavirus (COVID-19), you can furlough employees and apply for a grant that covers 80% of their usual monthly wage costs, up to £2,500 a month, plus the associated Employer National Insurance contributions and pension contributions (up to the level of the minimum automatic enrolment employer pension contribution) on that subsidised furlough pay.

You can obtain further information and make a claim online through GOV.UK.

The link below will allow you to workout the amounts you may be able to claim and the figures you will need to enter on the claim form:

HMRC Coronavirus Job Retention Scheme calculator

Working out what you can claim

The total grant for employer National Insurance contributions cannot exceed the total amount of employer National Insurance contributions you are due to pay. Therefore, adjust the total amount of employer National Insurance contributions by subtracting any Employment Allowance claimed in each pay period, this information will be on your payroll monthly summary reports.

Employee taxes

Your employees will still pay the taxes they normally pay out of their wages. This includes pension contributions (both employer contributions and automatic contributions from the employee), unless the employee has opted out or stopped saving into their pension.

Processing monthly payroll

The monthly payroll would be processed as usual to pay your furloughed employee(s) either 100% of their gross salary (including 20% top up salary) or only 80% of their usual gross pay (using HMRC’s calculator to obtain the correct figure) with the relevant employee(s) marked as “furloughed”.

You cannot claim for:

- additional National Insurance or pension contributions you make because you choose to top up your employee’s wages

- any pension contributions you make that are above the mandatory employer contribution

Please see the following post for further information on entering the payroll journals and how to process reclaimed SSP due to COVID-19:

How to process payroll and SSP COVID-19 Reclaims

How to process the COVID-19 Job Retention Scheme Payment Grant received from HMRC

Using HMRC’s calculator for following example of a furloughed employee below:

- Fixed monthly gross salary of £3,226.00

- Claim period: 1 March 2020 to 31 March 2020

- Furlough period: Started 1 March 2020

- They are paid every month

- Their National Insurance category is A, B, C or J

- They receive employer pension contributions as part of an automatic enrolment pension scheme

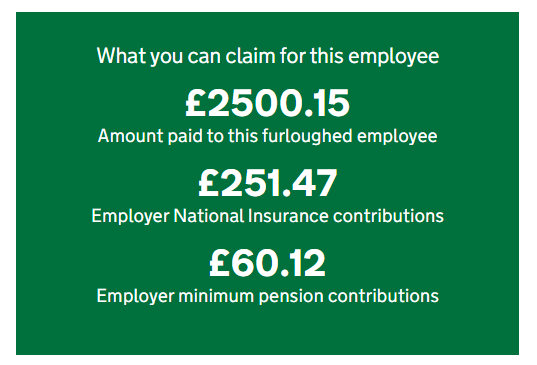

The calculation results are as follows:

Total Grant claimed = £2,811.74, the breakdown is shown below:

METHOD 1: GRANT PAYMENT ALLOCATED TO INCOME:

The simplest method is to tag the payment received to ‘Miscellaneous Income’ as shown below:

METHOD 2: GRANT PAYMENT ALLOCATED TO SPECIFIC EXPENSES:

This method would be used to ensure that the grant claimed is allocated against the specific expense on the nominal code.

- the above payment received would be tagged as ‘Something else not on this list’ to Gross Wages (7000), as follows:

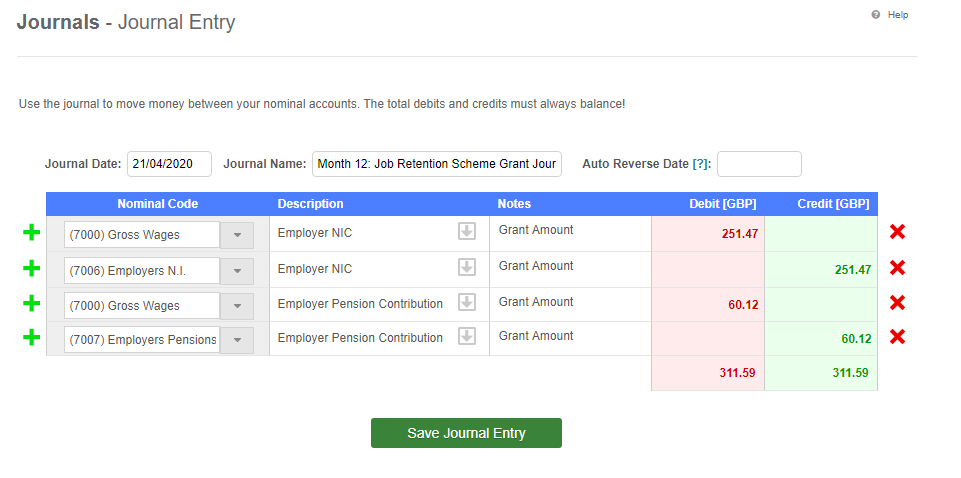

- Enter the following journals to allocate the Employer National Insurance contributions and Employer minimum pension contributions elements of the grant to the correct nominal codes:

The Chart of Accounts now shows the correct balances for the COVID-19 Job Retention Scheme Payment Grant received:

Once the payroll journals are entered, if not already done so, the nominal accounts will balance to Zero.

Using this method, at the Company’s year end your accountant will need to journal the grant received to ‘Misc Income / Grant Income’, therefore the following information can be provided to them and must be kept as confirmed by HMRC: After you’ve claim.

After you’ve claimed:

Once you’ve claimed, you’ll get a claim reference number. HMRC will then check that your claim is correct and pay the claim amount by Bacs into your bank account within 6 working days.

You must:

- keep a copy of all records, including:

- the amount claimed and claim period for each employee

- the claim reference number for your records

- your calculations in case HMRC need more information about your claim

- tell your employees that you have made a claim and that they do not need to take any more action

- pay your employee their wages, if you have not already