Hi Glen,

Did you get any feedback on the VAT reporting issue for the Flat Rate?

Hi Glen,

Did you get any feedback on the VAT reporting issue for the Flat Rate?

As you’re on flat rate VAT (FRV), you need to check the box ‘Allow VAT to be reclaimed on this purchase’ on the purchase invoice directly:

![]()

This will enable the VAT to be added to the purchase invoice and then reversed charged, make sure to enter the rate of VAT that would have been charged as if the purchase was made in the UK i.e. 20%:

If you need any further help, please let us know.

BUT what if it is not a capital purchases over £2,000?

@FaradayKeynes, it works in the same way, that box simply puts the figures into the VAT return.

If I tick box Allow VAT to be reclaimed on this purchase and pick vat rate (No vat) it wont pick figures in box 2 for reverse charge, if i pick vat rate 20% it still wont pick figures in box2 but box 4,7 &9 , it should only pick figures ion box 4 if it is capital expenditure fulfilling 2k conditions

Did you also tick:

20% VAT rate must be selected, as HMRC state “The value for VAT of any goods brought into the UK is the same as the value for VAT of the goods had they been supplied to you by a UK supplier”

Using 20% an example of the VAT return is shown below:

HMRC’s state under “10.8 How does the reverse charge affect accounting schemes?”:

“10.8.1 Flat Rate Scheme

Supplies to which the reverse charge applies are excluded from the Flat Rate Scheme. Any such supplies received and made should be accounted for under the reverse charge provisions.”

Whilst, in their guide “VAT Returns: how to complete your VAT Return box-by-box”, they confirm:

“Box 2: VAT due from you (but not paid) on acquisitions from other EU countries

You need to work out the VAT due - but not yet paid by you - on goods that you buy from other EU countries, and any services directly related to those goods (such as delivery charges). Put the figure in Box 2. You may be able to reclaim this amount, and if so remember to include this figure in your total in Box 4.”

In their “Flat Rate Scheme: how to complete your VAT Return box-by-box” they do not mention goods and state:

‘‘You also need to include any services you bought from abroad that the reverse charge applies to, and that you are entitled to claim back the VAT on - this will cancel out the figure you included in your Box 1 total.’’

As you can appreciate the rules can be complex, therefore it’s difficult for us to cover all scenarios and that’s why we have included the VAT adjustment tool:

Yes you are right, VAT is complex matter to deal with, without using VAT adjustment tools it wont give correct vat return e.g in case of good import from EU, system should not show any figure in box 4 unless capital 2k conditions are met and it is not picking up right % for flat rate on gross purchases either.

So for flat rate scheme one need to be very careful before submitting vat return

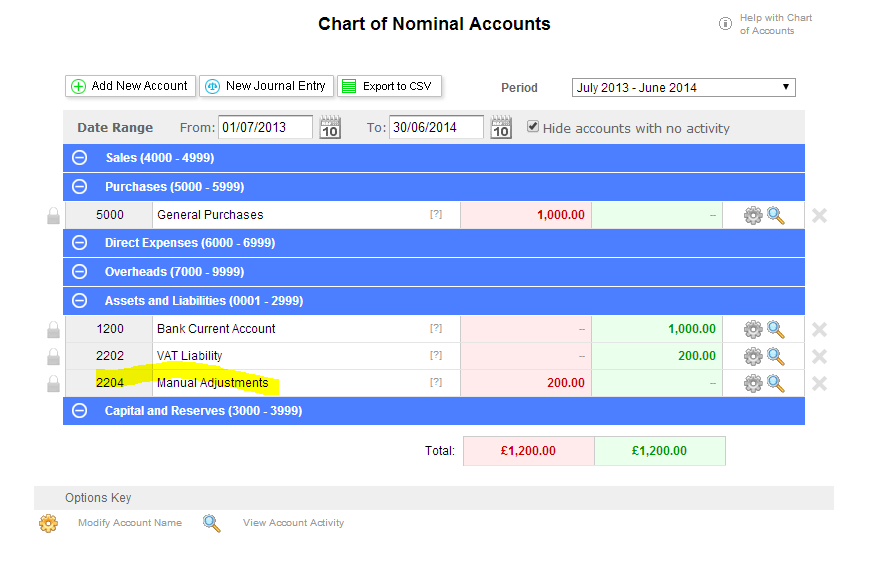

The adjustment for goods imported from the EU on the VAT return, unless capital 2k conditions are met, should be as follows:

A journal will also need to put through to move the VAT Manual Adjustment to gross up purchases:

Can you please provide us with an example so we can look into this.

what is your % on flat rate setting?

I’ve used an example rate of 13%

Should box 7 not show gross amount and box 2 should show gross time Flat rate %

for non flat rate its looking fine

Box 7 is correct and should show the VAT exclusive value. Box 2 is also correct and the standard rate of VAT and not the flat rate percentage must be used.

We appreciate your help in looking into this and other queries.

Oh i did not do the journal to gross up, if someone is buying quite a lot from EU then its lot of journals but then one should not be on flat rate if they are have to buy lot of stock from EU

Agreed, if they use different nominals for purchases, if they use general purchases then they could just journal the total figure at the quarter or year end.