Please Note: We have now added a dedicated cash based profit and loss report. Find out more here.

A standard Profit and Loss report is usually calculated on an invoice basis. This means that the income and expenditure is derived from the sales and purchase invoice dates and amounts, irrespective of whether they have been paid or not.

Sometimes it is useful to get a Profit and Loss breakdown that is linked to payments and receipts, this is referred to as a cash based Profit and Loss statement.

In 2017 we introduced a new Periodic Update Report to give users a glimpse into how income tax reporting will work under the new Making Tax Digital regime. Some businesses will need to report their income and expenditure on a cash basis so it made sense to extend support for a cash based Profit and Loss report.

Step by Step

Here’s how to create a cash based Profit and Loss Report for your business.

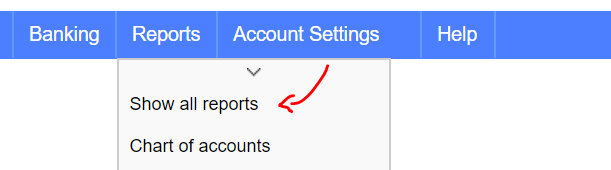

- Go to the “Reports” menu followed by “Show all reports”.

- Click on the “Making Tax Digital - Periodic Update” report.

- Within the report click on the “Settings” button and make sure the accounting method is on “Cash Basis”.

-

Save the settings and return to the main report page.

-

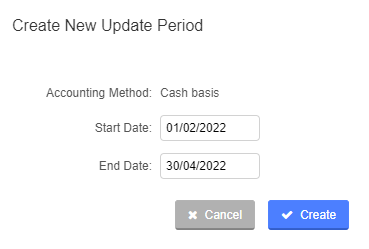

Click “New Update Period” and set the date range for which you’d like to report on.

-

Click on the “Create” button and wait for the report to be generated.

-

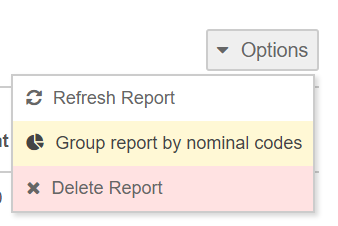

By default the report will be split into the standard MTD reporting headers for income and expenditure. Click on the “Options” button and select “Group report by nominal codes”.

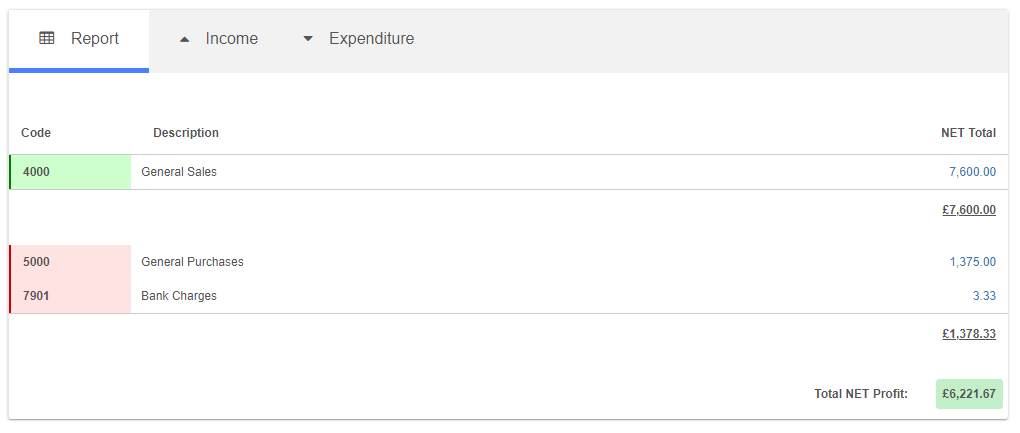

- You will now see a report that equates to a cash based Profit and Loss Statement.

These are snapshot reports so if you create, modify or delete underlying payments and invoices the report will not update unless you request a manual refresh. Nonetheless this tool should present a useful method to get a cash based overview of your income and expenditure that is grouped by nominal code.